N

on-bank lenders are taking a more proactive approach to troubled Chicago office buildings, suggesting that there may be hope for the sector's recovery. New York Life Insurance and National Real Estate Advisors have made recent moves at two distressed downtown properties, seizing them from borrowers instead of selling off non-performing loan notes.

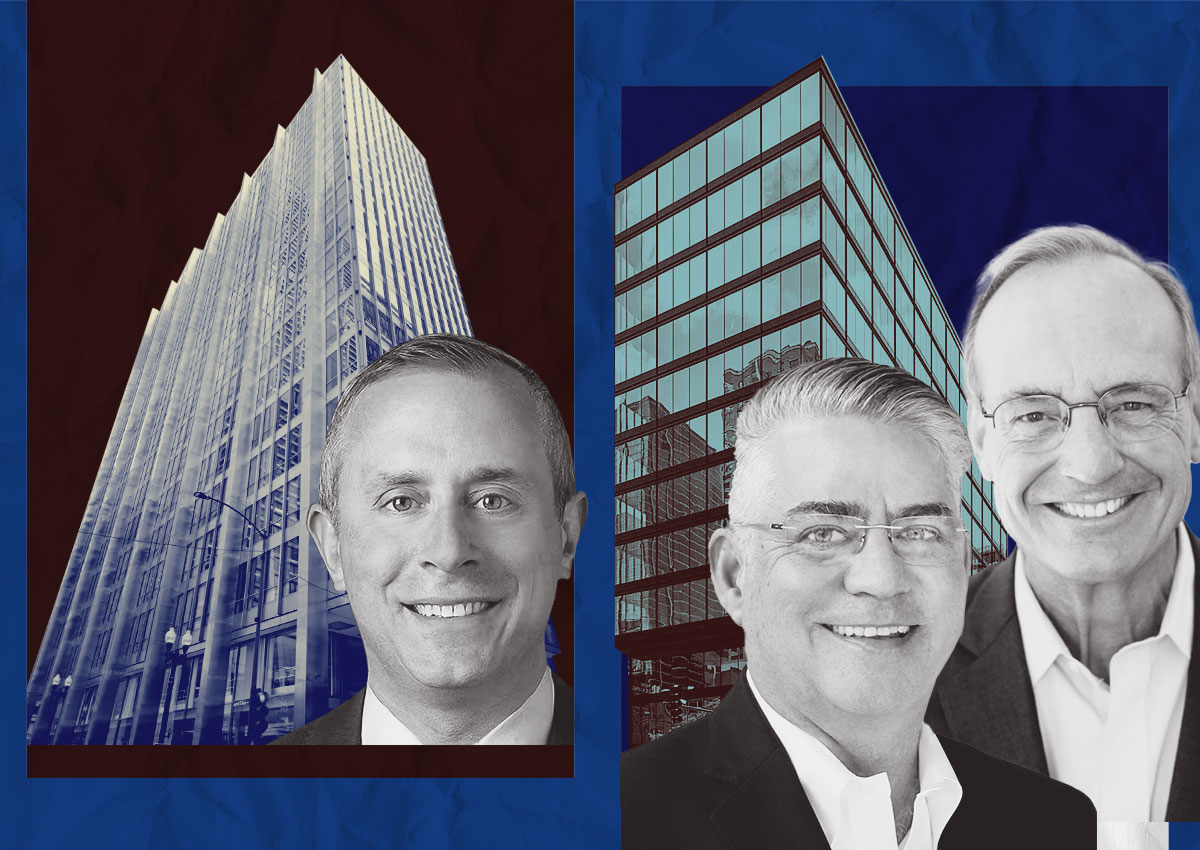

At 30 West Monroe Street, also known as the Inland Steel building, New York Life seized the property after exploring a sale of a $57 million non-performing loan note. The lender had initially refinanced the property in 2016 and is now working to lease up available space. Meanwhile, National Real Estate Advisors has started to plot a turnaround for 448 North LaSalle Street, which it seized last year from its developer after investing $70.5 million in the building's construction.

Rather than seeking a sale at a discount, National has hired brokerage Stream Realty to try to lease up the available space and is even investing in bringing new tenants into the building, including Electric Shuffle, a high-tech shuffleboard company with locations in several major cities. This approach suggests that lenders are open to putting more money into struggling properties to aid in their recovery.

Other lenders have preferred to let new buyers try to lead the sector's revival by seeking short-sales or loan note sales at discounts to face values. However, National and New York Life's recent moves may indicate a shift towards a more hands-on approach to managing troubled office buildings. "This is an extraordinary opportunity for businesses to establish themselves in one of Chicago's most dynamic submarkets," said Stream Realty's Mark Gunderson.